Bitcoin Faces Global Market Liquidity Steamroller – Bitcoin Magazine

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Liquidity Is In The Driver Seat

By far, one of the most important factors in any market is liquidity — which can be defined in many different ways. In this piece, we cover some ways to think about global liquidity and how it impacts bitcoin.

One high-level view of liquidity is that of central banks’ balance sheets. As central banks have become the marginal buyer of their own sovereign debts, mortgage-backed securities and other financial instruments, this has supplied the market with more liquidity to buy assets further up the risk curve. A seller of government bonds is a buyer of a different asset. When the system has more reserves, money, capital, etc. (however one wants to describe it), they have to go somewhere.

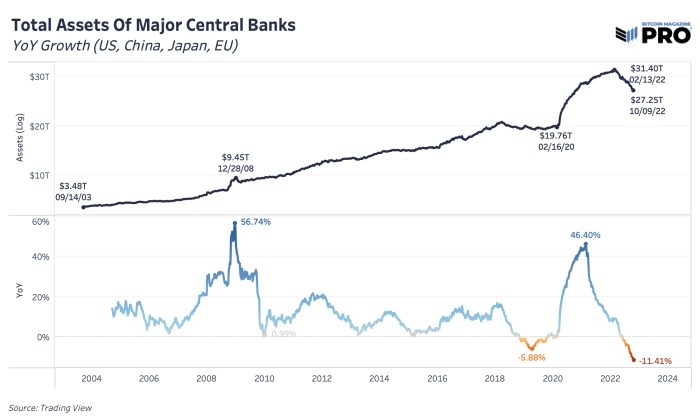

In many ways that has led to one of the largest rises in asset valuations globally over the last 12 years, coinciding with the new era of quantitative easing and debt monetization experiments. Central bank balance sheets across the United States, China, Japan and the European Union reached over $31 trillion earlier this year, which is nearly 10X from the levels back in 2003. This was already a growing trend for decades, but the 2020 fiscal and monetary policies took balance sheets to record levels in a time of global crisis.

Since earlier this year, we’ve seen a peak in central bank assets and a global attempt to wind down these balance sheets. The peak in the S&P 500 index was just two months prior to all of the quantitative tightening (QT) efforts we’re watching play out today. Although not the only factor that drives price and valuations in the market, bitcoin’s price and cycle has been affected in the same way. The annual rate-of-change peak in major central banks’ assets happened just weeks prior to bitcoin’s first push to new all-time highs around $60,000, back in March 2021. Whether it’s the direct impact and influence of central banks or the market’s perception of that impact, it’s been a clear macro driving force of all markets over the last 18 months.

There is a global attempt to wind down central bank balance sheets

At a market cap of just fractions of global wealth, bitcoin has faced the liquidity steamroller that’s hammered every other market in the world. If we use the framework that bitcoin is a liquidity sponge (more so than other assets) — soaking in all of the excess monetary supply and liquidity in the system in times of crisis expansion — then the significant contraction of liquidity will cut the other way. Coupled with bitcoin’s inelastic illiquid supply profile of 77.15% with a vast number of HODLers of last resort, the negative impact on price is magnified much more than other assets.

One of the potential drivers of liquidity in the market is the amount of money in the system, measured as global M2 in USD terms. M2 money supply includes cash, checking deposits, savings deposits and other liquid forms of currency. Both cyclical expansions in global M2 supply have happened during the expansions of global central bank assets and expansions of bitcoin cycles.

We view bitcoin as a monetary inflation hedge (or liquidity hedge) rather than one against a “CPI” (or price) inflation hedge. Monetary debasement, more units in the system over time, has driven many asset classes higher. Yet, bitcoin is by far the best-designed asset in our view and one of the best-performing assets to counteract the future trend of perpetual monetary debasement, money supply expansion and central bank asset expansion.

It’s unclear how long a material reduction in the Fed’s balance sheet can actually last. We’ve only seen an approximate 2% reduction from a $8.96 trillion balance sheet problem at its peak. Eventually, we see the balance sheet expanding as the only option to keep the entire monetary system afloat, but so far, the market has underestimated how far the Fed has been willing to go.

The lack of viable monetary policy options and the inevitability of this perpetual balance sheet expansion is one of the strongest cases for bitcoin’s long-run success. What else can central banks and fiscal policy makers do in future times of recession and crisis?

Relevant Past Articles:

Credit: Source link

Comments are closed.